Why The Psychology of Money Matters (To Real People)

FINANCIAL ADVICE | GUIDANCE | INSIGHTS | OBSERVATIONS

📖 WESTSTAR BOOK CLUB #1

I’ve read a lot of financial books over the years. Most focus on strategy, numbers, or predictions – all of which have their place. After all, money – whether we’re talking investments, personal finance, or business decisions – is often treated like a math problem: follow the data, plug in the formula, and you’ll know exactly what to do.

And that’s not entirely wrong. But it’s not the whole story, either.

Because in the real world, we don’t always make financial decisions with a spreadsheet. We make them in a meeting room, in the checkout line, or over dinner with people we love. And those decisions are shaped not just by what we know, but by what we feel.

That’s what makes The Psychology of Money by Seattle author Morgan Housel stand out.

It answers a question I’ve spent years exploring with clients: Why do smart people sometimes make not-so-smart financial decisions? And in the process, it shifts the conversation from what to do with your money to something even more important: why you do it that way in the first place.

TL;DR: Should You Read The Psychology of Money?

Yes – and don’t worry, it’s not a dry textbook.

If you’ve ever:

Wondered why sticking to your financial plan is harder than it sounds

Compared your financial choices or situation to someone else’s

Struggled to decide when the “right time” is to take action

… this book will feel both reassuring and eye-opening.

Housel writes in short, engaging chapters that feel more like stories than lectures. You can read a few pages and walk away with a new insight that sticks with you for days. Whether you’ve been investing for decades or are just starting out, it offers perspective that’s timeless.

Here are a few of the ideas from the book that continue to shape the way I think about planning, behavior, and what it means to build a life you actually enjoy.

Why Do Smart People Make Emotional Money Decisions?

The simple truth is that most financial decisions aren’t perfectly logical ones. It’s not about being good or bad at math – it’s that your choices are driven by your life experiences, your fears, your goals, and your memories. And those are all deeply personal.

So if it ever feels like you’re not being totally rational about money… that’s because you’re not. No one is. And that’s OK.

That’s also why it’s so important to understand your own money story.

History, emotions, and behavioral pitfalls can all shape our financial choices in surprising ways – especially when it comes to investing.

So in our practice, when we meet with a new client, we start there. We learn about their history and values, then explore together how they think and feel about money, how they respond to stress, and what their natural decision-making style looks like. That insight helps us shape a plan that doesn’t just look good on paper – it fits who they are and how they operate in real life.

Here are a few questions to help you explore your own financial story:

💭 What is your earliest memory of money?

💭 When do you feel most financially confident?

💭 What situations or conversations make you feel anxious about money?

💭 Whose opinion about your finances influences you the most?

How Do Luck and Risk Affect Financial Outcomes?

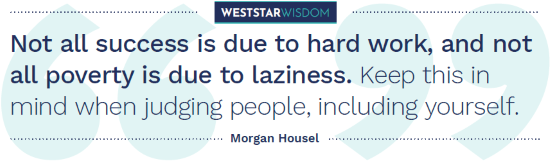

There’s a line in the book that has stuck with me:

It’s a powerful reminder that the outcomes we see – both our own and other people’s – aren’t always a reflection of skill or effort. Sometimes, they’re the result of timing, randomness, or decisions we almost made, but didn’t.

It’s also where we bump into a common thinking trap: the just-world fallacy, where we assume good outcomes come to good people – and misfortune is always deserved. This bias can be comforting, but it isn’t always true. And it can leave us feeling unfairly critical of ourselves when things don’t go our way, or dismissive of others in bad times.

This lesson feels especially relevant during times of economic uncertainty. When the market is volatile or headlines are scary, it’s easy to worry “Am I falling behind?” But sometimes, what you’re experiencing isn’t the result of a bad decision – it’s just part of the natural ebb and flow of the market, risk, and time.

What Makes a Financial Plan Actually Work?

The most successful financial plans aren’t the most aggressive or most complex – they’re the ones that people actually stick with, even when life gets messy. A reasonable plan followed consistently will almost always yield better results than a “perfect” one that gets abandoned under stress.

Or, as Housel puts it…

“Planning is important, but the most important part of every plan is to plan on the plan not going to plan.”

We’ve written before about how your mind can be your greatest financial asset or your greatest liability – and it’s a topic that’s just as relevant today. Life throws us curveballs like job changes, family transitions, and volatile markets. It’s only natural to respond to those things based on emotion and past experience. But those habits and internal narratives can either support your plan, or quietly sabotage it.

That’s not a reason to give up on planning – it’s a reason to plan for the real world.

So when we build a financial plan, our goal isn’t a rigid blueprint. It’s a framework that reflects your risk tolerance, your timeline, and your long-term goals. And most importantly, it’s built with the flexibility to evolve alongside your life.

What Is Money Really For?

When I ask clients what money means to them, their first answers are usually about buying power or security. But once we dig a little deeper, something else emerges – choice.

It’s about having the ability to say no to a job that drains you – and yes to an opportunity that excites you. It’s the space to take a break when you need it, the presence to be with those you care about, and the freedom to make a change when life calls for it.

That’s why this line from the book lands so well:

”Money’s greatest intrinsic value – and this can’t be overstated – is its ability to give you control over your time.”

I like to call that concept – knowing you have the ability to live life with intention, not reaction – “peaceful financial confidence”. That’s what financial planning is really about: not just how much you’ve accumulated, but what it enables you to do.

When Do You Know You Have “Enough”?

I’ve worked with many clients over the years who have done incredibly well for themselves, only to feel like it’s never quite enough. Not because they’re struggling, but because their expectations keep growing right alongside their success. A bigger number, a higher benchmark – the goalposts keep moving.

“Happiness is just results minus expectations.”

It’s a quiet kind of pressure, but it’s everywhere – especially in times when social media, fearmongering headlines, and economic uncertainty make it easy to feel like we’re either behind or about to be.

One of the ways we help clients to counter that mindset is by giving them the chance to pause and reflect. We help them to identify both the small and large goals they’ve already achieved. This could be paying off a mortgage, funding a college education, or taking a long-awaited vacation – anything where you can look at the progress you’ve made and say “I did it!”.

I talk a little more about this idea in this article on financial planning milestones, and I’d encourage you to read it if you have the time:

But the important takeaway is this: “enough” isn’t a number. It’s a feeling, found somewhere between future security and present satisfaction. So take a moment to look at your goals – not just where they’re headed, but what you’ve already accomplished. You might just find that right now, you’re already there.

Is Financial Comparison Holding You Back?

Whether it’s a neighbor’s shiny new car or a sunny vacation photo on Instagram, it’s easy to compare your financial life to someone else’s. And while there’s nothing wrong with enjoying nice things, the problem begins when we buy them just for external validation – to “keep up”, or because we want others to find us more likeable or impressive.

Housel calls this the “man-in-the-car paradox”: we think people admire us for our stuff, when in reality, they’re not really paying attention. They’re projecting their own desires onto what they see.

“You might think you want a fancy car or a nice watch. But what you probably really want is respect and admiration. And you’re more likely to gain those things through kindness and humility than horsepower and chrome.”

The truth is, it’s easy to look at someone else’s lifestyle and assume they’ve made it – but real wealth often looks quiet. The person driving the ten year old Elantra might be quietly sitting on decades of savings, and the one in the newest Ferrari may be one curveball away from financial trouble.

True wealth doesn’t need to be broadcast. It shows up in confidence and flexibility, not name brands and flash – and in goals that feel aligned, not performative.

How Can You Apply These Lessons in Your Own Life?

You don’t need to memorize economic cycles or predict market moves to feel financially confident. But what you can do is get curious about your mindset, and how that shapes the way you make choices when it comes to money.

Here are two reflection prompts to try this week:

💭 Track when you think about money – not when you spend it, but when it crosses your mind. What triggered the thought? A news story? A Conversation? A bill in the mail? Noticing your thought patterns is the first step toward understanding them.

💭 Think back to a recent financial decision you made (big or small). What was driving it? Safety? Freedom? Approval? Regret? The more clarity you have about your motivations, the more intentional your future choices will be.

Final Thoughts

The core lesson of The Psychology of Money isn’t a formula. It’s a mindset: that wealth is about how you live, not just what you earn.

Real financial well-being comes from knowing what matters to you, building a plan around it, and giving it (and yourself) room to grow – no matter what life may toss your way.

And good planning isn’t a rigid system, it’s a lifelong conversation: one that adapts to your story, your values, and your own version of “enough”.

If you’ve read the book, I’d love to hear what stuck with you. And if you’re curious how your own mindset might be shaping your plan, I’m always happy to talk.

-

Sam Gullette

Sam Gullette, CFP®, CLU®

Certified Financial Planner™

‘My mission in life is to help people take control of their money and avoid financial stresses. My clients are successful professionals and executives, many of whom are compensated heavily with company stock. Together we design plans to help maximize their wealth-building opportunities, provide strategies to minimize taxes, and help make sure their family is well cared-for if life throws them a curveball.’